During a parliamentary sitting in Port of Spain focused on approving the Standing Finance Committee’s report, Trinidad and Tobago’s Finance Minister Davendranath Tancoo made two key fiscal announcements that shape the country’s near-term economic and public policy trajectory. First, he confirmed that dedicated budget line items will be included in the 2027 national fiscal budget to cover all obligations finalized through ongoing collective bargaining negotiations with public sector worker unions, including those representing nurses and teachers. Addressing growing anxiety among union members waiting for negotiation outcomes, Tancoo noted that the full tabulation and quantification of outstanding settlement costs will take several more weeks to complete, assuring workers that promised relief will be formalized once the 2027 budget is introduced later this year. “Relief is coming, the documentation is being provided now and in fiscal 2027 the relevant appropriations will be made,” he stated to Parliament. Beyond the union negotiation announcement, Tancoo used the debate to defend the current administration’s request for an additional $2.9 billion in supplementary government funding, explaining the allocation is needed to cover urgent recurrent and capital expenditure obligations through September 30, 2026. He clarified that until a full new Appropriation Bill is tabled at the end of the current financial year, the supplementary funding will be allocated under existing expenditure heads, with administrative safeguards in place to keep all government operations running without disruption. Tancoo also used the parliamentary session to outline the current UNC administration’s economic progress over its first year in office, contrasting its performance with the former PNM government led by previous Finance Minister Colm Imbert. He emphasized that the current government has reversed years of sustained national economic decline within 12 months, acknowledging that global external shocks continue to shape domestic economic outlooks, impact investment conditions, drive cost-of-living changes and affect citizen livelihoods. “Governments are not judged by whether economic storms arise, but by how they respond,” Tancoo told the chamber. A core point of criticism directed at the previous administration was the 2010s closure of the Petrotrin state-owned refinery, which Tancoo labeled a critical strategic national asset. He argued its closure eroded the country’s energy security and forced increased reliance on more expensive imported refined fuel. Looking forward, he confirmed the current government will continue supporting the domestic energy sector, but will not rely on energy as the country’s sole long-term economic growth strategy. Tancoo also highlighted responsible management of the country’s Heritage and Stabilisation Fund (HSF), reporting that as of June 4, 2026, the sovereign wealth fund held US$6.6 billion in assets – a roughly US$620 million increase from the US$5.98 billion valuation recorded on April 30, 2025. Defending the $2.9 billion supplementary funding request, Tancoo emphasized the allocation is tied to active government programs, ongoing infrastructure projects and core public services currently being delivered to citizens. “The machinery of Government has accelerated, projects are being executed, and the nation’s development agenda is gaining momentum,” he said, noting the funding supports school repairs, critical infrastructure upgrades, public servant payrolls and institutional restoration. “Public servants are being paid. Obligations are being honoured. We are supplementing because we are delivering.” To counter opposition criticism of the supplementary request, Tancoo compared the current ask to supplementary funding approved under the previous PNM administration, noting that between 2016 and 2024, former Finance Minister Colm Imbert greenlit a total of $20.7 billion in expenditure increases, including $17.7 billion in additional draws from the national Consolidated Fund. He accused Imbert of hypocrisy, noting that what the previous government labeled standard fiscal practice is now being framed as irresponsible by the opposition. “The financial crises that this country has been placed in, must be bolted to his chest. He and the PNM are responsible,” he said. Tancoo then laid out key fiscal improvements delivered in the administration’s first year: when the UNC took office, the national fiscal deficit stood at $10.07 billion, equal to 5.8% of GDP; that figure has now been cut to $7.01 billion, or 4% of GDP – a nearly two percentage point reduction in just 12 months. Interest payments on national debt have also fallen from $7.13 billion under the PNM to $6.91 billion, freeing up additional resources for public investment rather than debt servicing. Most notably, the country’s primary fiscal balance has shifted from a $2.93 billion deficit under the previous government to a near-balanced position of a $101 million surplus, bringing Trinidad and Tobago to the threshold of a primary surplus after years of consecutive primary deficits. On the revenue front, Tancoo highlighted new revenue reforms introduced in the 2026 national budget designed to boost collection and strengthen long-term fiscal sustainability. Three new measures – the Commercial Bank Asset Levy, Electricity Surcharge, and Landlord Registration Fee and Business Surcharge – have generated approximately $224 million in new revenue since they launched in January 2026. Broader administrative and digital reforms are also underway, including modernization of the Inland Revenue and Customs and Excise Divisions and their information technology systems, the creation of a Real Estate Investment Trust (REIT) to monetize high-value state-owned assets, and preparation for the launch of NIF Bond 3 in September 2026. Work is also progressing on a new transfer pricing regulatory regime to improve tax compliance, boost foreign exchange earnings and strengthen the country’s external position. For the first seven months of the 2026 fiscal year (October 1, 2025, to April 30, 2026), total national revenue hit $30.1 billion, exceeding the original projection of $28 billion. Total expenditure came in at $31.8 billion, below the projected $34.5 billion, resulting in a deficit of approximately $1.7 billion for the period. Oil prices averaged US$62.09 per barrel in the first quarter of 2026 and US$77.64 in the second quarter, compared to the full-year budget assumption of US$73.25 per barrel, while natural gas prices averaged US$4.20 per MMBtu, matching initial projections. Tancoo acknowledged that first-half expenditure was inflated by long-outstanding liabilities, legacy debt and structural weaknesses inherited from the previous administration, including unpaid VAT bond obligations, delayed VAT refunds owed to local businesses, accumulated subsidy liabilities, and ongoing operational and financial challenges at state-owned enterprises. The minister also highlighted the administration’s progress in resolving long-stalled public sector wage negotiations, including a finalized settlement with the Public Services Association that delivered a 10% base salary increase for public servants. To ease immediate cost-of-living pressures, tens of thousands of public workers received one-time cash advances of between $10,000 and $20,000 against their retroactive back pay, with roughly $224.8 million disbursed across multiple sectors to date. Between October 1, 2025, and May 30, 2026, the government also spent $395 million on fuel subsidies to shield domestic consumers from volatile global energy price increases. Updated projections for the remainder of the 2026 fiscal year forecast average oil prices of US$85 per barrel and natural gas prices of US$4.50 per MMBtu, up from the original budget assumptions. Combined with other adjustments, these higher commodity prices are expected to boost total annual revenue by $381.7 million, resulting in a projected full-year fiscal deficit of $7.0 billion. Tancoo confirmed the $2.9 billion in supplementary expenditure will be financed through a mix of domestic and external borrowing, including partnerships with major multilateral development institutions.

分类: business

-

Antigua and Barbuda strengthens global MICE positioning

The twin-island Caribbean nation of Antigua and Barbuda has launched a targeted, multi-pronged strategic initiative to strengthen its position as a premier global destination for Meetings, Incentives, Conferences, and Exhibitions (MICE), a high-growth segment of the international tourism and business travel landscape.

Against a backdrop of post-pandemic recovery in global business events, where destinations worldwide are competing aggressively to capture corporate and organizational travel spending, Antigua and Barbuda is leaning into its unique combination of geographic appeal, modern infrastructure upgrades, and personalized service offerings to carve out a distinct niche. Government tourism officials and private sector stakeholders have partnered to roll out a series of improvements, including expanded venue capacity at major conference centers, upgraded digital connectivity for hybrid events, and new incentive packages designed to attract small to mid-sized corporate retreats, regional industry summits, and international non-profit gatherings.

Unlike large, crowded MICE hubs in major metropolitan areas, the nation’s selling point lies in its combination of business productivity and post-event leisure opportunities, with white-sand beaches, luxury resort accommodations, and a stable, welcoming political environment that appeals to event organizers seeking a distraction-free yet memorable setting for their gatherings. Officials note that growing the MICE segment delivers outsized economic benefits compared to traditional leisure travel, as MICE attendees typically spend 2-3 times more per visit than regular tourists, generate off-peak occupancy for hotels, and create high-quality local jobs in hospitality, event management, and transportation.

The push also includes targeted marketing campaigns at major global MICE trade shows, including ITB Berlin and IMEX America, where the destination is highlighting its new incentives such as tax breaks for international event organizers, streamlined visa processing for attendees, and dedicated event planning support teams to reduce logistical burdens. Industry analysts point out that this strategic move aligns with broader global trends in the MICE sector, where more organizations are seeking unique, less crowded destinations that offer both value and a high quality of experience for attendees.

-

CBvS wil burgers beter voorbereiden op digitale financiële toekomst

Paramaribo, Suriname – The Central Bank of Suriname (CBvS) has kicked off a three-day international gathering of global financial policymakers in Paramaribo, centered on a core mission: strengthening the financial resilience of ordinary Surinamese citizens and upgrading consumer protection frameworks for a fast-digitizing national economy.

This event marks the 31st in-person Consumer Empowerment & Market Conduct Working Group Meeting hosted by the Alliance for Financial Inclusion, running from June 15 to 17 at Paramaribo’s Hotel Torarica. This year’s gathering carries the overarching theme of Advancing Gender Equity and Empowerment, bringing together policy representatives from dozens of developing nations to share on-the-ground insights and actionable strategies around three critical pillars: expanded financial inclusion, robust consumer protection, and responsible public financial policy.

Vanessa D’Costa-Chehin, head of the Financial Inclusion & Education division at CBvS, told attendees that meaningful financial inclusion extends far beyond simply opening a basic bank account for unbanked populations. In an era of rapidly scaling digital financial services, she argues the most pressing challenges lie in building public financial literacy and putting proactive consumer safeguards in place. “We cannot keep pushing financial innovation without centering the needs and safety of consumers,” D’Costa-Chehin explained. “Financial services must be secure and inspire public trust. Consumer protection is non-negotiable as we expand access to digital financial tools across the country.”

Financial education is framed as a foundational component of CBvS’s broader inclusion strategy. Dion Mokkum, an IT specialist working with the central bank, emphasized that early preparation for responsible financial decision-making is key to empowering younger generations. Outreach initiatives like the global Global Money Week campaign, he noted, play a critical role in teaching young people core habits around saving, entrepreneurial planning, and responsible money management from an early age.

Andrew Baasaron, Suriname’s Minister of Economic Affairs, Entrepreneurship and Technological Innovation, reinforced the government’s commitment to building a secure, trustworthy digital financial ecosystem. He highlighted that efficient, accessible payment systems are a lifeline for the country’s small and medium-sized enterprises, stressing that the benefits of national economic growth must reach small business owners and everyday citizens, not just large corporate entities.

These priorities align directly with the CBvS’s ongoing policy agenda. Through two key frameworks – the updated National Financial Inclusion and Education Strategy (NFIES) action plan and the national Payment Strategy 2026-2030 – the central bank is working to deliver faster payment infrastructure, secure digital identification solutions, and expanded access to formal financial services for all populations, including communities in remote inland areas of Suriname that have long been underserved by traditional financial institutions.

CBvS Governor Maurice Roemer, speaking at the official opening of the summit, reiterated that financial technology and innovation must ultimately serve the needs of all Surinamese society. “At its core, financial inclusion is about people,” Roemer said. “It is about entrepreneurs looking to grow their small businesses, farmers in remote regions gaining access to the financial tools they need, women and young people gaining stronger footing to participate in the national economy, and families building greater long-term financial security for their households.”

Beyond facilitating global knowledge sharing between developing nations, the summit serves as a launching pad for CBvS’s next phase of policy work: building a more inclusive, secure, and accessible financial system that delivers tangible benefits to all residents of Suriname.

-

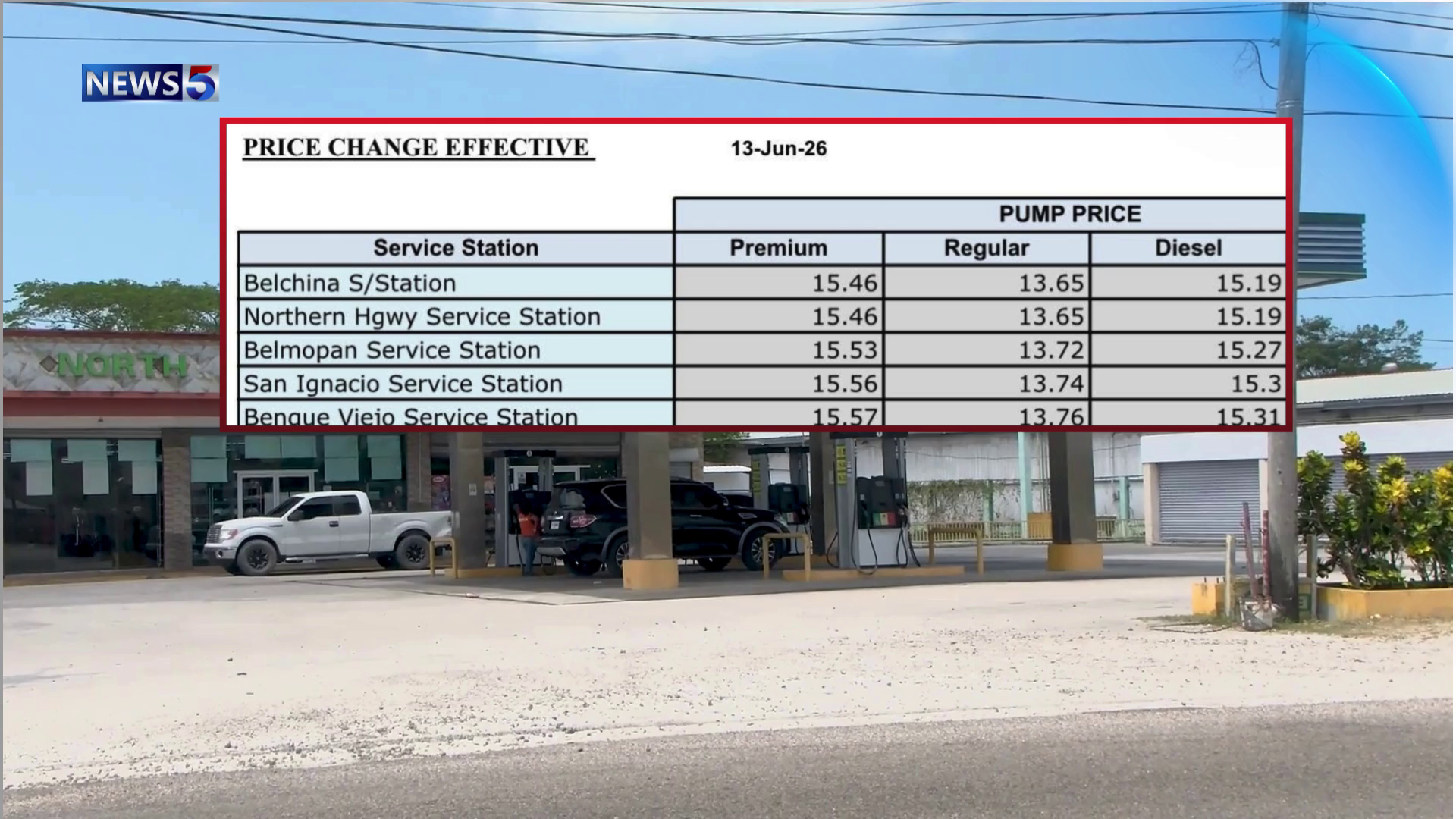

Price Drop at Pumps Follows Overseas Deal

After months of unrelenting upward pressure on retail fuel prices that squeezed household budgets and raised transportation costs across Belize, motorists finally saw a much-anticipated reprieve at gas pumps starting Saturday, June 14, 2026. In Belize City, the per-gallon price of regular unleaded fuel dropped by $1.18, landing at a new retail rate of $13.65 per gallon. In a surprise to some industry observers, premium grade gasoline and diesel have held steady at their current price points: premium remains $15.46 per gallon, while diesel stays at $15.19 per gallon in the city, as of the latest adjustment.

This sudden local price cut follows a major international development that has shaken global energy markets: unconfirmed but widely circulated reports indicate that the United States and Iran have reached a breakthrough agreement to end ongoing conflict and reopen the Strait of Hormuz, one of the world’s most critical chokepoints for global oil trade. The strait has been closed to large-scale commercial oil shipping for an extended period, creating major supply chain disruptions that drove up crude oil prices on global markets for months. The reported deal has already triggered a broad, global downturn in crude oil costs, which is now being passed through to retail consumers in Belize.

Local energy analysts note that the full impact of this international agreement on Belize’s fuel prices will depend on how the deal is implemented in the coming weeks. This news organization will continue monitoring developments on both the international diplomatic front and local retail fuel prices to bring audiences the latest updates.

-

Governor: BiMPay transactions will remain free

Against a global backdrop of rapid digital transformation in financial transactions, the Central Bank of Barbados has moved to calm public uncertainty around the future of physical cash, confirming on Monday that the island nation will not implement a mandatory shift to a fully cashless economy. Central Bank Governor Dr. Kevin Greenidge made the clarification during a press briefing addressing the launch of BiMPay, Barbados’ new nationwide instant digital payment system, which went live last Friday.

Greenidge emphasized that while cash will retain its status as legal tender and remain in permanent circulation, the growing adoption of convenient digital platforms like BiMPay is expected to trigger a gradual, organic decline in cash usage over time. He pointed to successful instant payment infrastructure rollouts across major global markets as a precedent, noting that systems such as Brazil’s Pix, India’s Unified Payments Interface (UPI) and Thailand’s PromptPay all led to a natural reduction in cash reliance without government mandates forcing out physical currency.

“Where you have a convenient alternative, people naturally shift away from cash,” Greenidge explained. “Look at markets like China, India and Kenya — once scanning QR codes for payment becomes widespread, many merchants prefer digital transactions, and consumers opt for them out of convenience. Today, the average person carries debit cards, credit cards, digital wallets and a small amount of cash; people will naturally choose the option that works best for them, and many will decide cash is bulky and unnecessary, that shift just doesn’t need to be forced.”

In its first 48 hours of operation, the BiMPay platform processed roughly 20,000 transactions totaling nearly $8 million, marking a strong early uptake of the new infrastructure by Barbadian consumers and businesses.

Beyond addressing concerns about the future of cash, Greenidge also moved to dispel growing public fears that participating financial institutions would introduce new transaction fees for BiMPay use. The governor stressed that peer-to-peer and consumer-to-business transactions on the platform will remain permanently free, and any bank seeking to implement fees must first secure formal approval from the Central Bank, which he has no intention of granting for these transaction types.

“Central Bank remains the primary regulator for this payment system, and we have not stepped back from that role,” Greenidge said. “Person-to-person and person-to-business transactions on BiMPay will stay free, that policy is not changing, and no financial institution can alter that without our sign-off.”

Greenidge also highlighted the transformative potential of BiMPay for small and micro businesses across Barbados, noting that the platform removes cost barriers that have historically locked many small operators out of card-based digital payments. Traditional credit card processing requires expensive point-of-sale terminals that carry ongoing fees, putting that infrastructure out of reach for many small proprietors such as local rum shop owners. With BiMPay, any business can simply download the mobile app and generate a free QR code, allowing customers to scan and pay directly into the merchant’s bank account at no cost.

“This system saves small businesses money that they would otherwise spend on terminal fees, and it also lets them avoid missed sales from customers who don’t carry enough cash,” Greenidge added. “That accessibility is core to what we want this platform to deliver — inclusive growth that supports small operators across the country.”

-

BiMPay moves nearly $8m in first weekend despite early issues

Barbados’ first national instant payment infrastructure, BiMPay, has delivered a solid performance in its first 48 hours of public operation, Central Bank of Barbados Governor Dr. Kevin Greenidge confirmed in a Monday press briefing held at the bank’s Grand Salle. In the two days since the system went live over the weekend, it has processed more than 20,000 transactions totaling nearly $8 million, with a 99% success rate that puts early performance well above expectations for a newly launched fintech platform.

Despite the overall strong showing, Greenidge acknowledged that the rollout hit predictable early-stage “teething issues”, most notably widespread registration difficulties reported by hundreds of users on social media just hours after BiMPay launched Saturday. The governor explained that the overwhelming majority of registration blocks stemmed from an unforeseen interaction with Google’s spam protection systems. In the first hour after launch alone, the BiMPay app was downloaded more than 12,000 times, and a large share of those users registered with Gmail accounts. The sudden volume of verification emails sent from BiMPay’s domain triggered Google’s automated anti-spam defenses, which blocked all outgoing verification messages from the platform, leaving users unable to receive the access codes required to complete registration.

Greenidge noted that prior stress testing ahead of launch could not have predicted this specific outcome, as there was no way to anticipate that such a large majority of early registrants would use Gmail accounts or that Google’s security protocols would flag the verification traffic as malicious. Central Bank teams quickly contacted Google to resolve the issue, and the block was cleared within hours, allowing affected users to complete their registration. Greenidge added that most other early issues have either been fully resolved or are on track to be fixed imminently.

Of the less than 1% of total transactions that failed in the first two days, Greenidge attributed all problems to minor formatting errors, such as incorrect entry of account or branch numbers, rather than fundamental flaws in the BiMPay infrastructure. “This is an extremely strong success rate for a newly launched system,” Greenidge emphasized. “Nearly 99% of 20,000 transactions worth $8 million went through without a hitch, across all participating financial institutions. The system is working exactly as it was designed to.”

Another ongoing adjustment involves the process for retrieving BiMPay access tokens from users’ financial institutions. Currently, users must obtain a unique token from their bank to access BiMPay, either via text, email, or their existing online banking portal. Most participating institutions have opted to host token access through their existing banking apps, but not all have placed the BiMPay token link prominently on their homepage as required. The Central Bank has held multiple meetings with chief executives of participating institutions over the past two days to address this, and is working with all providers to add a clearly labeled “BiMPay Token” button or link to their homepage for easy access.

When pressed for details on the total development and launch cost of BiMPay, Greenidge declined to share a specific figure, but clarified that the project did not draw on taxpayer funds. As an operationally and financially independent institution, the Central Bank of Barbados funds the initiative through its own investment portfolio, rather than government allocations.

Greenidge framed BiMPay as a critical public good for the Barbadian economy, noting that no single domestic financial institution had the scale to develop and roll out a universal instant payment system on its own, given the country’s small size. The upgrade to the national payments infrastructure, he argued, will strengthen Barbados’ economic standing and position the country to capitalize on upcoming regional and domestic development opportunities.

Looking ahead to the second phase of BiMPay rollout, which will onboard additional financial institutions and government agencies including the National Insurance and Social Security Service (NISSS), the Central Bank has declined to set a firm launch date. Deputy Governor Michelle Doyle explained that rigorous standardization of payment data formatting across all new participating entities is a non-negotiable prerequisite for expansion. Without aligned data standards, Doyle noted, there is an increased risk of transaction failures that could undermine user trust in the system. The Central Bank will first complete detailed preparatory work with all prospective new partners to ensure full data standardization, and will only announce a launch date once onboarding preparations are fully complete. “We are prioritizing long-term functionality over a fast rollout,” Doyle explained, “to make sure the entire system works seamlessly for all users when we expand.”

-

Masterclass waarschuwt: olie-inkomsten alleen garanderen geen welvaart

On June 15, a landmark first masterclass focused on Suriname’s upcoming Savings and Stabilization Fund brought together cross-sector stakeholders in Paramaribo’s Hotel Torarica, with industry and policy experts united in a core message: the fund’s long-term success will depend not on the total volume of incoming oil and gas revenues, but on the quality of its management, transparency, and governance structures.

Organized jointly by the Youth Education and Leadership Foundation (YELF) and the Suriname Energy Chamber (SEC), the event gathered representatives from government, the private sector, academia, labor unions, and the national energy sector to deliberate on the fund’s critical role in sustainably managing future natural resource revenues for the South American nation, which has emerged as a new oil and gas producer in recent years.

Opening the masterclass, Minister of Oil, Gas and Environment Patrick Bruinings noted that Suriname is still in the early stages of building its national resource fund framework. While Norway’s widely celebrated sovereign wealth fund is often held up as a global gold standard, Bruinings emphasized that even Norway’s management system evolved gradually over decades, adapting to new research and changing economic conditions, meaning Suriname must build a model suited to its own context through ongoing learning.

Lead presenters Karel Eckhorst and René Abrahams explained that enacting formal legislation to establish the fund is only the first critical step. Equally important is strengthening the government institutions tasked with implementing the Savings and Stabilization Fund law, most notably the Ministry of Finance and Planning, which will oversee core operations of the fund.

Experts further stressed that the fund does not operate in isolation; it is an integrated component of Suriname’s broader public finance system. This means strong regulatory frameworks alone are not enough. The nation also needs to modernize its national budget process, build specialized capacity for evidence-based policy development, and ensure active sustained engagement from civil society across all stages of fund management.

A core design feature of the Surinamese model is a requirement that all fund assets be invested overseas. This structural choice is intended to avoid the disruptive economic impacts that can occur when large volumes of natural resource revenue flood directly into the domestic economy, including rapid currency appreciation and inflation. Returns generated from these international investments will then be allocated to national development priorities through formal budget rules.

Attendees also left the masterclass with a clear warning: the fund on its own cannot shield Suriname from economic volatility or the common pitfalls of resource dependence. To avoid the so-called “Dutch disease” – a condition where resource booms crowd out growth in other non-resource sectors – the nation must continue prioritizing broad economic diversification. Experts identified investments in micro, small, and medium-sized enterprises, general education, knowledge development, and vocational skills training as essential foundations for long-term inclusive, sustainable growth.

The masterclass also traced the decades-long origins of Suriname’s national savings fund idea. As early as the 1970s, policy thinker Frank Essed first highlighted the critical importance of prudent management of natural resource revenues for the nation. That vision was later advanced and expanded by figures including Karel Eckhorst and former Staatsolie director Rudolf Elias, leading to the current push for formal establishment of the fund.

In closing remarks, SEC Chair Orlando Olmberg reaffirmed the fund’s core ultimate purpose: to deliver long-term economic stability and sustained shared prosperity for current and future generations of Surinamese people. Echoing the event’s central message, he warned that no institutional fund can offset the damage of poor governance. “The success of the fund will ultimately not be determined by the size of the assets it manages, but by the quality of the governance that oversees it,” Olmberg stated. For future oil and gas revenues to genuinely advance Suriname’s national development, he added, prudent financial management, full transparency, and broad civil society engagement are irreplaceable non-negotiable conditions.

-

Hospitality training scheme draws nearly 3 000 applicants in three months – Govt

Barbados’ push to expand its critical tourism economy is receiving a strong early response from job seekers, as a new government-led workforce development program has pulled in nearly 3,000 applicants in just three and a half months, according to the country’s Minister of Technical and Vocational Training.

The Barbados Hospitality Gateway Training Initiative (BHGTI), a state-backed program designed to close the growing labor gap in the island nation’s hospitality sector, was originally framed to train up to 5,000 new workers. The initiative comes as local hospitality leaders have repeatedly flagged growing difficulty sourcing qualified candidates to fill hundreds of open roles across the sector.

Nine new hotels are scheduled to open in Barbados in the near term, creating demand for an additional 4,000 trained hospitality workers, Minister Sandra Husbands confirmed in public comments. That looming labor shortfall is what has driven the government’s targeted dual focus: supporting construction of new hotels and residential tourism properties, while building a pipeline of trained workers ready to step into new roles once the properties open.

Husbands explained that the BHGTI is structured to be fully demand-driven, a design feature intended to ensure trainees exit the program with skills that align directly with open industry positions. To achieve this, the vocational training department partners closely with the Ministry of Labour to conduct regular labor market assessments that map unmet skill needs, and adjusts training curricula and cohort sizes accordingly. For example, if the market already has enough bellhops and has a shortage of professional chefs, the program will shift enrollment to prioritize culinary training over other roles.

“This flexible structure gives trainees near certainty that a job opportunity will be waiting for them once they complete their training,” Husbands said. The overarching goal of the program, she added, is to create a closed, supportive ecosystem that boosts employment rates and lifts earning potential for young Barbadians and working families across the island.

In response to the unexpected flood of applicant interest, the government has moved quickly to expand training capacity. The program was initially hosted at three existing vocational institutions, but those facilities did not have enough physical space to accommodate the volume of interested trainees. To resolve the gap, officials have partnered with the Ministry of Education Transformation to secure access to 10 additional public school facilities, allowing the program to scale up enrollment and meet the high demand from prospective workers.

-

Bajans mixed on BiMPay as opinions shape early response

Just days after Barbados’ latest digital payment infrastructure BiMPay made its official debut, public opinion across the island has fractured sharply, with residents debating whether the platform will redefine the future of commercial transactions or remains a confusing service that many have yet to fully grasp. While early adopters have already praised the platform for its unmatched convenience in cross-bank instant money transfers, a significant share of the public is taking a wait-and-see approach. Many of these observers question whether the tool aligns with their unique daily needs, while advocates warn that marginalized and vulnerable populations must not be sidelined as the country transitions to more digital financial services.

Katelia Murrell is among the first users fully won over by BiMPay’s functionality, saying it resolves a longstanding hassle she encountered regularly when sending money. “It’s noticeably more convenient for people like me who need to send funds to contacts that don’t share the same bank provider,” Murrell explained. She already tested the platform just one day after it launched, noting that “I used it once literally last night, and it was honestly incredibly straightforward to use.”

What left the strongest impression on Murrell was the unprecedented processing speed. “The platform said it would take 10 seconds, but I swear the transfer went through even faster than that,” she said. “When we tested the reverse transaction, where the recipient sent money back to me via the platform’s QR code feature, everything worked perfectly without any glitches.”

For self-employed worker Shaquille Hewitt, BiMPay offers a promising solution to the constant frustrations he faces when receiving customer payments. “As someone who works for themselves, it’s always been a headache dealing with cross-bank transfers or checks drawn on institutions other than my own,” Hewitt said. “I’m optimistic this platform will streamline that whole process and make it far less stressful.”

Other residents welcome the government’s push for digital financial innovation but have emphasized that policymakers must prioritize inclusion as Barbados expands its digital transaction ecosystem. “There need to be alternative options for people who can’t use BiMPay, especially older adults who don’t have digital literacy or people who don’t own a compatible smartphone,” said Holford Walrond. “Everyone needs to be able to access their money easily, that’s my main concern. Even though I support what the government is trying to do, keeping choice available to consumers is absolutely essential. If the government sees this as the right path forward for Barbados, that’s fine, they’re making a good effort to modernize our financial system. But I still firmly believe people should get to choose how they manage their money.”

Rico Simpson, who has already completed the sign-up process and is preparing to activate his account, says BiMPay clears key hurdles that limit existing digital payment services. “I already signed up for BiMPay, I just haven’t activated it yet,” Simpson said. “I chose to join because I see it as a really convenient way to send transfers, similar to CIBC First Pay, but with much more flexibility. With that existing service, you have to be a CIBC customer and have your cell number linked to the account to use it. But with BiMPay, you don’t even need a traditional bank account number to use it — you can hold all your funds directly in the BiMPay app itself, which I think is a big advantage.”

For Joseph Cummins, the main barrier to adoption is not opposition to digital innovation, but a lack of clear personal understanding of how the service would work for him. “It’s hard for me to wrap my head around it right now because I haven’t gotten the chance to dive into the details yet,” Cummins said. “The information is out there, but I need to do my own research to figure out how it fits into my own financial life, especially how it interacts with the banking services I already use to manage my money.”

Even so, Cummins acknowledges that BiMPay carries meaningful broader benefits for Barbados’ financial inclusion. “People who operate outside the traditional formal banking system will get an opportunity to join the formal financial ecosystem and use that access to improve their lives,” he noted. Still, he remains unsure whether the platform will lead him to change his own long-standing money management habits. “I keep wondering how it will affect me at my age, since I’m pretty set in my ways and only really use my current bank for things like paying bills. The big question for me is: does this actually impact my daily life? Will it make sense for me to change my habits to start using it? Right now, that’s still unclear to me.”

At Bridgetown’s Pelican Village craft hub, Sandra Padmore, owner of souvenir business Nafai Creations, says her customer base makes her decision to adopt BiMPay far from straightforward. “I’m still thinking it over, I haven’t tried it out yet,” Padmore said. “My main question is that my shop caters almost entirely to tourists. If BiMPay is mostly built for local users, I’m not sure it makes sense for me to adopt it. We barely get local customers coming through these souvenir shops, so that’s got me a bit confused. Most tourists pay with credit or debit cards anyway, and I already have a card terminal set up. I just need more clarity on how this would benefit my business specifically.”

Barbados Prime Minister Mia Mottley has emphasized that BiMPay was designed specifically to serve small business owners and informal vendors, creating a faster, more inclusive system for sending and receiving payments across the island. But on the streets of Bridgetown, as vendors and everyday residents weigh whether to add the new platform to their financial tools, the debate has less to do with the technology itself and more to do with core tradeoffs: convenience against long-held familiarity, innovation against broad accessibility, and whether a system billed as the future of payments can actually work for every single Barbadian.

-

Food security push hinges on private investment, Munro-Knight says

As the Caribbean grapples with a rapidly expanding food import bill that drains critical economic resources, regional leaders are calling for transformative, large-scale private investment to reverse deepening import dependence and kickstart long-term economic restructuring. In a keynote address at the opening of the Regional Food Systems Investment Forum held at Barbados’ Hilton Resort, Barbados’ Agriculture Minister Dr. Shantal Munro-Knight emphasized that incremental, small-bore changes will never deliver the systemic shift the region urgently needs.

Decades of growing reliance on foreign-sourced food has left the Caribbean with a staggering import burden, a trend Dr. Munro-Knight highlighted as a clear wake-up call for an ambitious, investment-centered overhaul of regional food systems. She tied this call to the Caribbean Community (CARICOM)’s landmark 25 by 25 target – an initiative designed to cut the region’s food import bill by 25% by 2025, later expanded with additional goals – noting that the framework was born from a shared recognition that food security demands bold, unified action.

Official data underscores the severity of the challenge: over a recent three-year period, total Caribbean food and agricultural imports hit $13.76 billion, a sum equal to roughly 5% of the region’s entire annual gross domestic product. “That’s not small, that’s not insignificant,” Dr. Munro-Knight told attendees, stressing that the current trajectory is economically unsustainable for small island developing states across the region.

A core part of the minister’s message was a call to reframe how the public and investors view Caribbean agriculture. For too long, she argued, the sector has been reduced to small-scale production and subsistence farming, but it must now be repositioned as a modern, high-potential economic sector packed with lucrative investment opportunities. “The dialogue around food systems has moved beyond just production,” she explained. “What we have come here to talk about today is a conversation that revolves around one of the most significant economic and development opportunities that the Caribbean has to offer.”

Unlike narrow traditional farming frameworks, modern regional food systems span an entire value chain: from logistics and agro-processing to cold storage infrastructure, digital innovation and agricultural technology. Dr. Munro-Knight pointed out that expanding investment across these interconnected segments not only creates strong returns for private investors but also directly strengthens the region’s long-term food security. “When we think about food systems, we have to break out of that traditional frame,” she said. “We can challenge ourselves, and we can look at the big investable opportunities that are there.”

Drawing a parallel to the landmark Bridgetown Initiative, which has reshaped global conversations around climate financing, Dr. Munro-Knight outlined the critical role governments must play in unlocking private capital for food system development. She emphasized that governments are meant to act as catalytic partners, working to “crowd in private capital” rather than bearing the entire burden of investment themselves.

But for private investment to flow at the needed scale, the minister stressed that investors require stable, transparent governance. “Capital needs surety. It needs governments that have clear policies, clear pathways, frameworks, that are transparent and data-driven,” she said.

Dr. Munro-Knight also highlighted technological innovation as a game-changing lever for cutting import dependence. She noted that targeted investment in tech-driven agriculture and modern farming solutions could improve the region’s food production balance by up to 15%, a major gain toward meeting the 25 by 25 target.

In Barbados, this commitment to transformation is already taking shape through the national Strategic Crop Escalation and Production Plan, which prioritizes expanding domestic output of 15 high-demand staple crops. The minister also spotlighted the proposed Barbados-Guyana Food Terminal as a flagship example of the large-scale investment opportunities available. The $25 million infrastructure project, she explained, will leverage Barbados’ strategic geographic location to build a regional logistics hub, strengthen cross-island food distribution networks, and support broader efforts to build a more resilient, self-sufficient Caribbean food system.