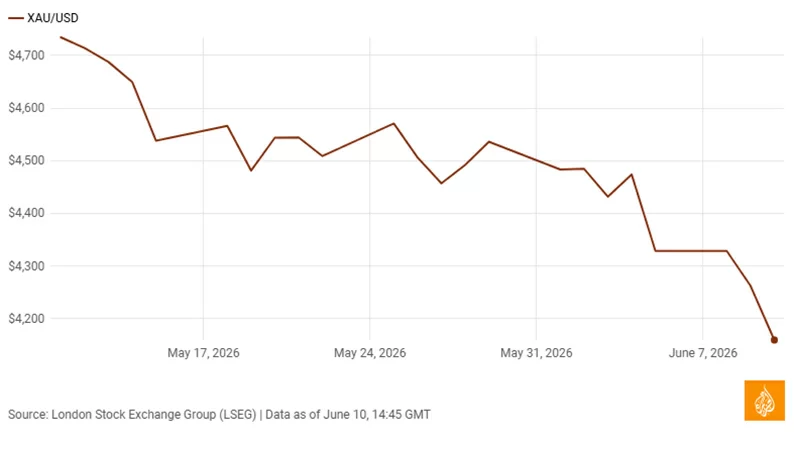

Global gold prices have dropped below the key $4,160 per ounce threshold, hitting the lowest level recorded in 2026, in a striking departure from the traditional market behavior that sees safe-haven assets rally during periods of global geopolitical crisis. The downward pressure on gold prices began in late February 2026, when the United States and Israel launched military operations against Iran, marking the start of a months-long regional conflict. In typical crisis scenarios, investors flood into gold as a stable hedge against inflation and market volatility, but the current cycle has flipped this long-held pattern on its head. Since the military campaign began, gold has retreated dramatically from its January 28 peak of $5,303 per troy ounce, closing at $4,235 per troy ounce last Friday. Market analysts point to persistent high inflation and shifting central bank interest rate expectations as the core drivers of this unexpected trend. The root of the current inflation surge traces largely to disruption at the Strait of Hormuz, a critical global chokepoint for oil and natural gas shipments. In retaliation for the outbreak of war, Iran has blocked commercial shipping traffic through the strait, sending global energy prices soaring and pushing inflation rates far above central bank targets across major developed economies. In the United States, annual inflation currently sits at 4.2%, the highest reading in three years. At the same time, the country’s labor market has remained surprisingly stable, erasing investor hopes that the Federal Reserve would move to cut interest rates in the near term. While gold is widely viewed as a reliable hedge against rising consumer prices, higher interest rates typically create significant downward pressure on the precious metal. Unlike interest-bearing assets such as bonds or dividend-paying stocks, gold is classified as a non-yielding asset – it generates no passive income beyond its inherent intrinsic value. Investors can only earn returns from gold if its market price rises over time, putting it in direct competition with higher-yielding assets when interest rates climb. “As an asset, gold is as close as you can get to holding physical cash,” explained Justin Cardwell, chief options analyst at OptionSpreaders.com. “It pays no dividends, and you only see capital gains when its market price goes up. People buy gold purely to bet on its price appreciation.” Cardwell added that when interest rates rise, gold loses much of its investment appeal, as investors pivot en masse to higher-yielding dollar-denominated assets. The ongoing conflict with Iran has also had the unintended effect of strengthening the U.S. dollar, and because gold is globally priced in dollars, the two assets have historically moved in opposite directions. “When the dollar strengthens, gold comes under pressure; when the dollar weakens, gold usually climbs. Right now, the dollar is strong, and gold is feeling that pressure,” noted Collin Plume, CEO of Noble Gold Investments. Looking ahead, the future trajectory of both the dollar and gold remains deeply uncertain, as market expectations for monetary policy have shifted dramatically in just a few months. “The biggest question for the rest of this year – and likely for the next several years after that – is what comes next,” Plume said. “A few months ago, markets were pricing in interest rate cuts, which would have lifted gold prices and boosted asset values across the board. That outlook has completely changed. Now we’re facing headwinds, including a real possibility that the Federal Reserve will actually raise rates instead of cutting them. Every asset class is affected by this shift, but gold is particularly sensitive to interest rate movements.” Before the outbreak of the war with Iran, former President Donald Trump had pushed aggressively for steep interest rate cuts from the Federal Reserve. But according to the CME FedWatch Tool, which tracks market expectations for Fed rate decisions, the probability of a rate hike by December 2026 now stands above 50%, a shift that will almost certainly continue to weigh on gold prices, Plume said. “Interest rates and inflation are like two opposite ends of a seesaw, and gold sits right in the middle,” Plume explained. “What’s unique about 2026 is that we’re seeing both high inflation and expectations of higher rates at the same time – and right now, the interest rate side is winning. That’s why gold is facing such strong downward pressure.” Late last week, news emerged of a potential negotiated settlement between the United States and Iran to end the conflict. In response to that development, gold closed slightly higher on Friday than it had the previous day. Cardwell noted that news of a potential end to the war would ultimately be positive for gold prices, as markets would expect energy-driven inflation to cool in the wake of a reopened Strait of Hormuz. Even so, he cautioned that any meaningful shift in gold’s trajectory would take months to play out. “Gold’s current price level is likely acting as a support floor,” Cardwell said. “Even if the war ends, there are still so many other overlapping factors that are holding gold prices in check right now.”