Paramaribo, Suriname – The Association of Economists of Suriname (VES) has raised sharp questions over the methodological approach the current administration has used to calculate its projected 2026 national budget deficit, arguing that the actual gap between public spending and revenue is far larger than the government has reported. According to VES Secretary Swami Girdhari, the real deficit will reach 7.7% of gross domestic product (GDP), not the 5.1% officially claimed by the Surinamese government.

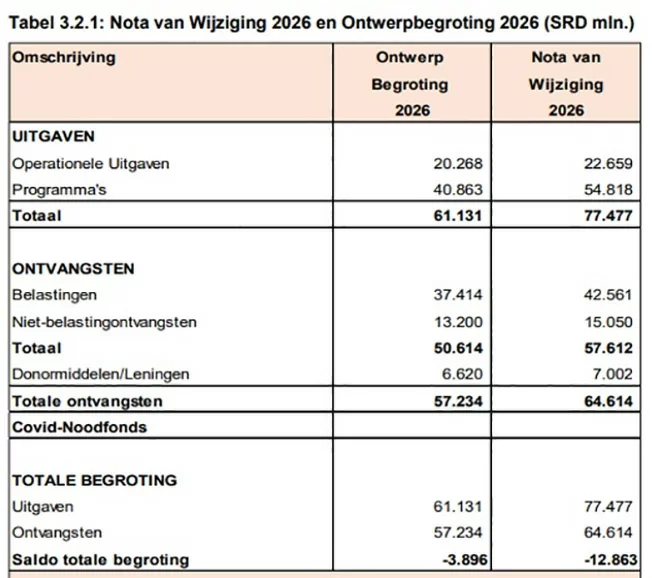

The Council of Ministers gave its approval to the 2026 Amended Budget Memorandum on May 21, which outlines total projected public spending of 77.4 billion Surinamese dollars (SRD) against total projected revenue of 64.6 billion SRD. Under the government’s calculation framework, this results in a deficit of 12.8 billion SRD, which equals 5.1% of the 252.2 billion SRD official projected GDP for 2026.

Girdhari, in an interview with local outlet Starnieuws, noted that the biggest red flag is the sharp upward revision to the 2026 GDP estimate. As recently as September 2025, official projections put national GDP at roughly 180 billion SRD. The new 252.2 billion SRD estimate represents a 40% increase in just nine months. Even after accounting for projected annual inflation of roughly 10%, the implied real GDP growth comes out to nearly 30% – a figure Girdhari says lacks clear justification. “The question is whether this level of growth is realistic,” Girdhari said. “The Ministry of Finance and Planning needs to provide the public with a full breakdown of the underlying calculations that led to this estimate.”

A core point of VES criticism centers on the government’s classification of borrowed funds as regular revenue. Per the amended budget, the government expects 42.5 billion SRD in direct and indirect tax revenue and 15 billion SRD in non-tax revenue, totaling 57.5 billion SRD in baseline receipts. The administration then adds 7 billion SRD in new loans to hit the 64.6 billion SRD total revenue figure.

This accounting approach is fundamentally incorrect, Girdhari argues. “Loans are not revenue – they are financing instruments that increase the state’s future debt obligations, and should never be counted as regular operating income,” he explained. When the 7 billion SRD in new loans is excluded from revenue in line with standard international budget accounting rules, the actual financing gap grows to nearly 20 billion SRD, pushing the deficit up to the 7.7% of GDP the VES estimates. The association emphasizes that international fiscal standards require a clear separation between regular revenue streams (including taxes, non-tax receipts, and grants) and financing sources such as loans and reserve withdrawals, noting that this distinction is required to produce a transparent, accurate picture of the government’s true fiscal position.

VES also warns that financing the deficit and meeting existing debt obligations remains a major unaddressed risk for 2026. The current budget framework leaves the government heavily dependent on new borrowing to cover a large share of planned spending, and 9.4 billion SRD in existing debt repayments are scheduled for next year. The association is calling for the publication of an up-to-date debt sustainability analysis to give the public a complete view of the country’s overall fiscal standing, saying the government has not yet explained how it will meet its existing debt repayment obligations.

Beyond 2026, VES has raised concerns over the government’s medium-term fiscal projections included in the budget’s Medium-Term Fiscal Framework, which covers the 2026 to 2030 period. The government projects steady growth in both revenue and spending over the five-year window, with budget surpluses emerging between 2027 and 2029, growing to 9.6 billion SRD by 2029. However, the framework projects a return to deficit in 2030, with a shortfall of 9.9 billion SRD.

Girdhari calls this swing from a nearly 10 billion SRD surplus to a nearly 10 billion SRD deficit in just one year – a 20 billion SRD shift – extremely unusual. He notes that the shift is driven almost entirely by soaring debt repayment requirements: scheduled debt repayments rise from 9.3 billion SRD in 2029 to 32.3 billion SRD in 2030. This jump is tied to the November 2025 debt restructuring agreement, which requires Suriname to repay roughly $1 billion in 2030. “In practice, this shifts a massive financial burden onto the administration that takes office in 2030,” Girdhari said.

Finally, the association is warning against excessive optimism around anticipated future oil revenue, which appears to underpin much of the current budget framework. VES says the government risks implicitly counting unearned future oil income in its current spending plans, despite the fact that these revenues have not yet been realized. Girdhari pointed to global precedent showing that countries that increase public spending before commodity revenues actually materialize often face severe fiscal crises when output or prices fall short of projections.

To address these risks, VES is calling for strict fiscal discipline, full public transparency around all budget calculations, a robust savings and investment strategy for future resource revenues, and strong institutional safeguards to reduce the impact of politically driven budget cycles that prioritize short-term spending over long-term fiscal stability.