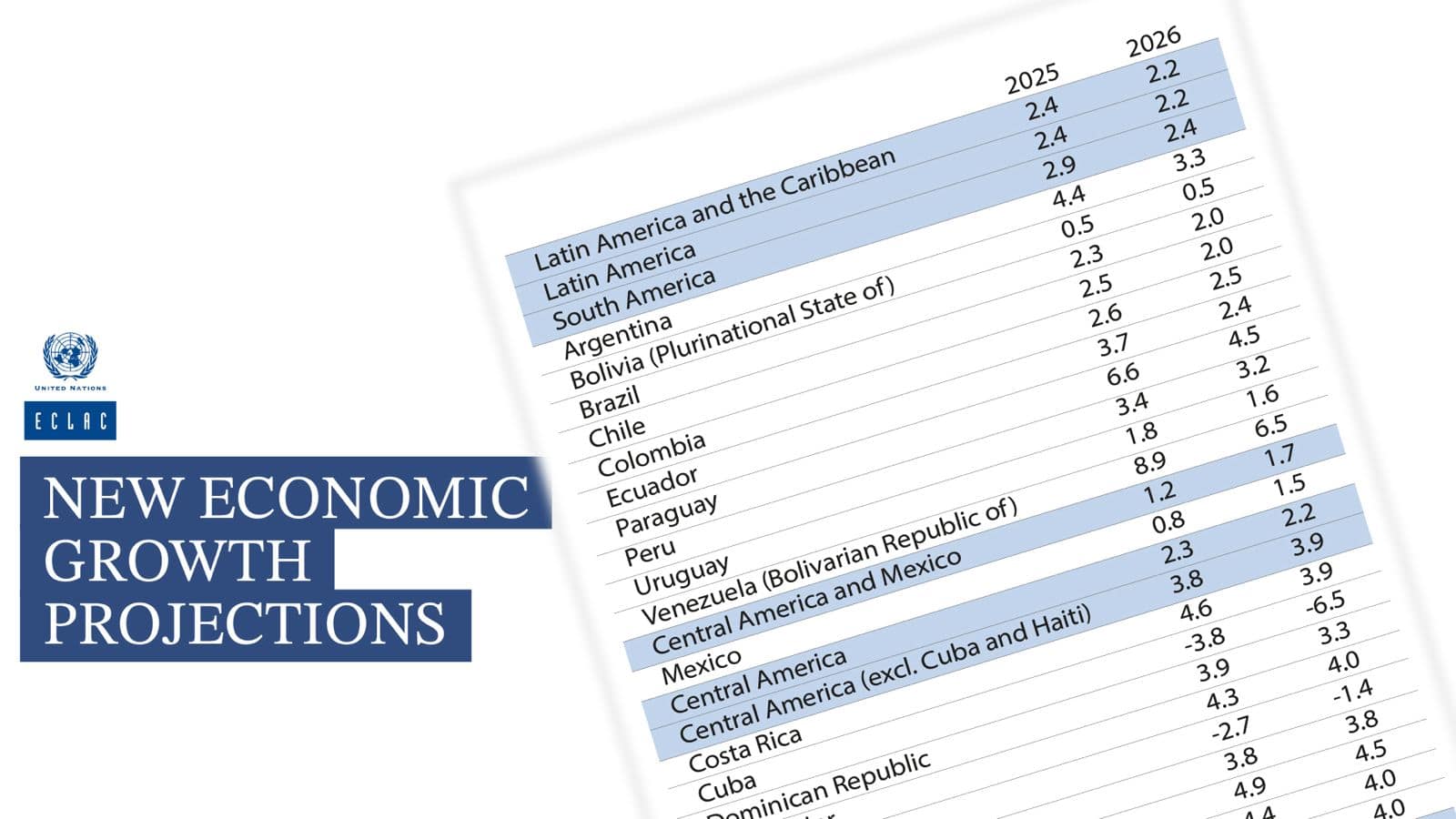

New updated economic projections from the United Nations Economic Commission for Latin America and the Caribbean (ECLAC) have trimmed the 2026 average growth outlook for the region’s economies to 2.2%, a slight downward adjustment from the 2.3% forecast published in December 2025. The revision comes as the global operating environment has grown far more challenging than analysts anticipated at the end of last year, marked by escalating geopolitical frictions, tighter-than-expected global financial conditions, and a renewed surge in inflationary pressures across the world.

ECLAC’s analysis notes that this slowdown in economic momentum will be felt across nearly the entire region. Of the 33 economies tracked in the report, 24 will see growth decelerate in 2026, while only seven are projected to register an acceleration in output. If the forecast holds, the region will mark four consecutive years of growth hovering around 2.3%, a trend that underscores deep-rooted low growth capacity across Latin America and the Caribbean.

The degradation of the global external landscape stands out as the primary driver of the lower forecast. Between January and April 2026, rising geopolitical tensions and ongoing conflict in the Middle East have amplified uncertainty across global financial and commodity markets, stoking widespread volatility. Most notably, the average price of West Texas Intermediate (WTI) crude oil in the first three weeks of April 2026 was 74% higher than the average recorded in December 2025. This sharp jump has fanned broad global inflationary pressures and pushed up production and transportation costs for economies around the world, including those in the Latin American and Caribbean region.

The oil price shock has been compounded by rising global food prices, a simultaneous growth slowdown in the region’s largest trading partners — including the euro area, China, and India — and a general cooling of international trade. The World Trade Organization (WTO) projects that the volume of global goods and services trade will expand by just 2.7% in 2026, down from a 4.7% expansion in 2025. Against this backdrop of persistently higher inflation and softening trade prospects, the world’s major central banks have adopted more cautious monetary policy stances, keeping financial conditions significantly tighter than were forecast at the end of 2025.

Beyond global headwinds, muted domestic aggregate demand is also acting as a drag on regional growth. The largest constraint on expansion remains underwhelming private consumption. While fixed investment has shown early signs of a nascent recovery, growth in capital spending remains moderate across most of the region’s economies. A slowdown in activity that emerged in the second half of 2025, particularly in the region’s largest economies, has carried over into 2026, extending the trend of weak performance.

As economic activity cools, job growth across the region is also expected to moderate. ECLAC projects regional employment will grow by roughly 1.1% in 2026, down from 1.5% growth in 2025. At the same time, imported global inflation is pushing up domestic price levels across the region: the median inflation forecast for 2026 now tops 3%, up from 2.4% in 2025. South American economies are disproportionately affected by this trend, facing continued pressure from exchange rate volatility and higher costs for imported inputs and transportation.

The report also highlights sharp heterogeneity in economic performance across different countries and subregions. In total, just nine economies are projected to grow by 4% or more in 2026, eight will see growth between 3% and 4%, 13 will expand at a rate below 3%, and three economies are expected to contract.

Broken down by subregion, South America is forecast to grow 2.4% in 2026, down from 2.9% growth in 2025, with most economies in the subregion seeing deceleration. Central America will see a slight easing of growth to 2.2% in 2026 from 2.3% in 2025, a result dragged down by expected contractions in Cuba and Haiti; excluding those two economies, the subregion’s average growth would tick up to 3.9% from 3.8% in 2025. The English- and Dutch-speaking Caribbean is projected to hit 5.6% growth in 2026, a tiny uptick from 5.5% in 2025, driven almost entirely by strong expansion in Guyana; excluding Guyana, the subregion’s average growth would fall to 1.2% from 2.0% in 2025.

ECLAC warns that significant downside risks remain to the current forecast, and any materialization of these risks could lead to further downward growth revisions. Key risks include the persistence of restrictive global financial conditions, continued inflationary pressure from elevated energy and food prices, ongoing volatility in international commodity and financial markets, widespread vulnerability to external shocks, and persistent weak domestic demand across much of the region. In some economies, long-standing structural weaknesses including external financing constraints, limited fiscal and monetary policy space, and fragile institutional frameworks could further drag on performance.

The current economic landscape lays bare the core structural challenges holding the region back: persistently low trend growth, excessive exposure to global external shocks, and an urgent need to strengthen domestic growth engines. ECLAC emphasizes that expanding mobilization of both domestic and external resources, paired with improvements in governance, will be critical to advancing policy frameworks that boost investment, lift productivity, and strengthen macroeconomic resilience amid an increasingly uncertain global environment.