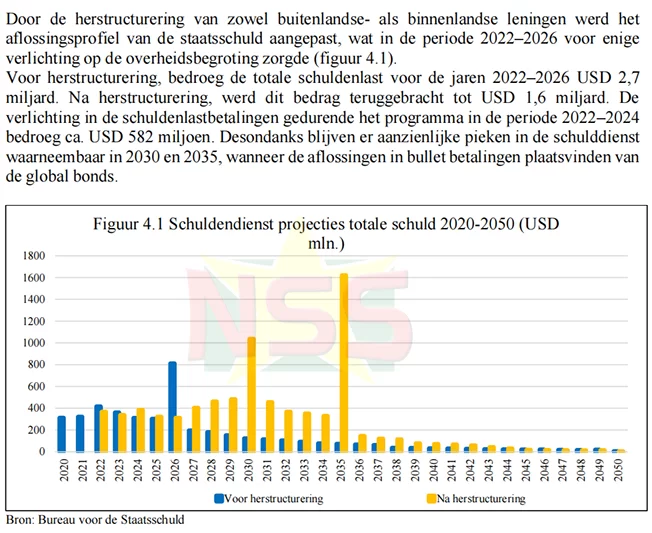

New data released in Suriname’s 2026 Public Debt Plan reveals that the South American nation’s total sovereign debt reached 189.9 billion Surinamese dollars, equal to approximately $4.9 billion, by the close of 2025. Hefty near-term debt repayment obligations that were originally scheduled for 2025 have been restructured and pushed out to 2030 and 2035, according to the document from Suriname’s Public Debt Office.

Official statistics from the General Bureau of Statistics (ABS) put the country’s debt-to-GDP ratio at 129.6% as of the end of 2025. Calculated under the methodology used by the International Monetary Fund (IMF), that ratio stands at a lower but still elevated 108.7%. Total scheduled debt service for 2026 is currently projected at 15.7 billion Surinamese dollars, equal to roughly $405 million at current exchange rates.

The Public Debt Office outlines several key drivers behind the ongoing rise in Suriname’s national debt. These include the disbursement of new cross-border loans, a major recapitalization effort for the Central Bank of Suriname (CBvS), the inclusion of the Value Recovery Instrument in the national debt portfolio, and growing backlogs in overdue payments to domestic government suppliers.

Breaking down the total debt balance, more than $4.1 billion of the total is classified as external obligations to international creditors, while roughly $823 million consists of domestic debt held by local institutions and investors. Close to 90% of all Suriname’s sovereign debt is denominated in foreign currencies, a structure that leaves the country’s public finances highly exposed to sudden exchange rate swings that can increase the local currency cost of repayments overnight.

Over the course of 2025, Suriname concluded nearly $2 billion in new loan agreements with a range of global and regional development institutions. A large share of these new arrangements went toward refinancing existing expensive debt, but the country also secured new development financing targeted at key economic sectors and infrastructure projects.

Among the new development funding, the Saudi Fund for Development provided a $20 million loan to expand and upgrade Suriname’s energy generation and power distribution infrastructure. The Inter-American Development Bank (IDB) allocated $25 million to support the country’s struggling aviation sector. The World Bank contributed more than $22 million to fund climate adaptation projects and flood risk reduction initiatives across the country. In March 2025, the IMF also disbursed the final $44.6 million tranche of funding under Suriname’s ongoing economic reform program supported by the fund.

The largest single financing transaction of 2025 closed in November, when Suriname launched $1.575 billion in new international bonds with 5-year and 10-year maturities, alongside a $300 million dedicated social bond. Proceeds from this issuance are primarily earmarked for refinancing maturing legacy debt and clearing outstanding past payment obligations.

Despite the current elevated debt burden that weighs heavily on the national budget, Suriname’s government projects that the country’s debt position will improve steadily over the medium term. The optimistic outlook is tied to forecasts of broad economic growth, rising foreign direct investment in the country’s emerging offshore oil sector, and the expected start of commercial crude oil production from 2028 onward.

A formal debt sustainability analysis conducted by the government projects that these developments will push the debt-to-GDP ratio back below the legal national debt ceiling of 60% by 2029. Until that milestone is reached, however, public debt servicing will remain one of the biggest spending pressures on the Surinamese government’s annual budget.