Suriname’s economy expanded in the first quarter of 2026, but the country still faces persistent structural headwinds including sticky double-digit inflation and unsustainably high public debt that threaten long-term stability, the Suriname Economic Oversight Board (SEOB) warned in its latest quarterly economic bulletin published July 3.

The board’s data shows economic activity continued to pick up steam through the first three months of the year, with the Monthly Economic Activity Index (MEAI) climbing from 5.6% annual growth in January to 6.3% in March. This growth was driven primarily by expanding activity in the trade, hospitality, public administration, and a range of other service sectors. However, key industries including mining and transportation lagged behind broader growth trends, highlighting uneven performance across the Surinamese economy.

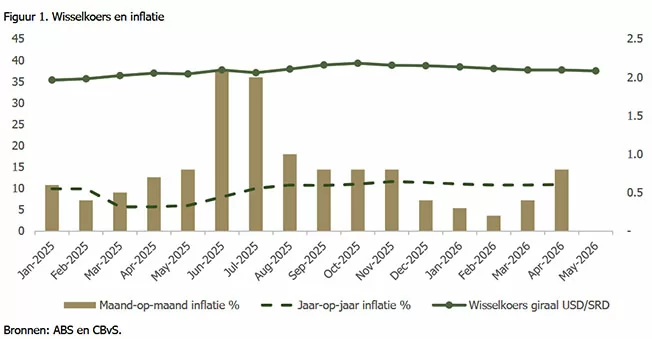

Most notably, SEOB flagged that inflation has reaccelerated after recent improvements, pushing the annual rate back above the 10% threshold. Annual inflation hit 10.9% in April, while monthly inflation doubled from 0.4% in the previous month to 0.8%. This sustained double-digit inflation continues to erode household purchasing power and push up operating costs for domestic businesses, creating widespread financial pressure across all segments of the economy, the board noted.

There were some bright spots in the report, however. The local exchange rate remained relatively stable through April and May, with the U.S. dollar trading consistently around 37.5 Surinamese dollars (SRD) and the euro hovering near SRD 43.8 at the end of May. The country’s international reserves also held at a robust $1.88 billion, enough to cover 7.7 months of imports – far above the widely accepted international benchmark of 3 months of import coverage.

Public finances also posted a positive surprise in January, with the central government recording a fiscal surplus: total revenues hit SRD 6.6 billion, while expenditures came in at SRD 4 billion. Even so, SEOB stressed that one month of positive results does not signal a structural recovery in public finances, and the overall fiscal position remains fragile.

The most significant long-term risk highlighted in the bulletin is the country’s massive public debt. As of March, total public debt reached 86.9% of gross domestic product (GDP) under Suriname’s legal calculation framework, and 123.3% of GDP when measured by international standards. Both figures are far above the threshold widely considered to signal a sustainable debt load for emerging market economies.

The domestic banking sector remained a bright spot in the report, with SEOB confirming the system remains stable overall. Banks maintain adequate capital buffers to absorb potential shocks, and the share of non-performing loans remains low at just 3.1% of total outstanding loans. Even so, average lending rates remain high at 14%, which continues to dampen private sector investment and slow broader economic expansion, the board added.

To address these ongoing challenges, SEOB put forward a series of policy recommendations for the Surinamese government. Key priorities include maintaining strict fiscal discipline to rebuild fiscal sustainability, expanding and strengthening the country’s social safety net to protect households from inflation, increasing government transparency and implementing stronger anti-corruption measures, and fully activating the national Savings and Stabilization Fund to manage future expected oil revenues. The board also recommended divesting from non-strategic loss-making state-owned enterprises, bringing the country’s new public procurement law into force, and doubling down on policies to drive economic diversification, expand non-mining exports, and attract investment outside of the traditional mining sector.