A fresh debate over the future of Antigua and Barbuda’s temporary windfall tax has erupted following a June 2026 opinion piece calling for the policy’s extension and expansion to advance national education goals. Responding to Professor C. Justin Robinson’s argument that the proposal deserves full national deliberation, a veteran policy analyst with over 35 years of decision-making experience has pushed back against the rushed framing of the conversation, while calling for greater transparency and dispassionate cost-benefit analysis before any final policy vote.

The analyst emphasizes that effective problem-solving does not prioritize being seen as correct, but rather making the right, contextually informed decision. A robust decision-making process requires first defining clear, measurable outcomes, diagnosing why current systems are falling short, evaluating emerging trends and alternative solutions, and only then deliberating on a path forward. In the analyst’s view, the current conversation around the windfall tax has inverted this process: the solution—extending and expanding the levy—has been presented to the public before any clear consensus on the underlying problem has been established.

While the analyst acknowledges alignment with some of the equity-focused education outcomes Professor Robinson aims to achieve, they reject the windfall tax as the appropriate funding mechanism. They also note a structural conflict of interest: Professor Robinson is affiliated with the University of the West Indies (UWI), the primary beneficiary of the tax revenue, so full objectivity on the policy cannot reasonably be expected.

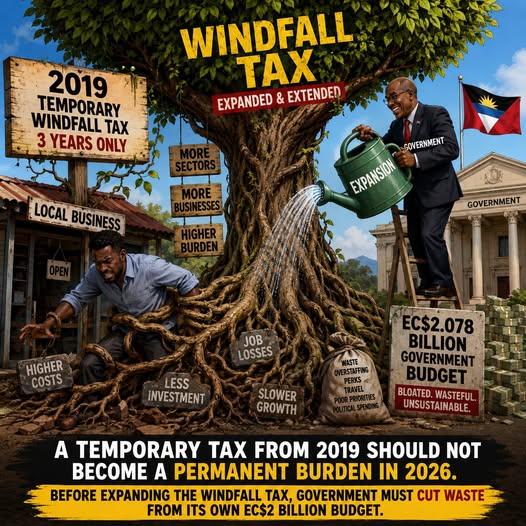

For context, the windfall tax was first introduced in 2019 as a three-year temporary measure to fund the construction of UWI’s Five Islands Campus. Levied at a 10% rate on net profits, it applies exclusively to private businesses operating in banking, telecommunications, insurance, and petroleum distribution—on top of the existing 25% corporate tax already paid by these firms. Despite its original temporary mandate, the government has repeatedly extended the tax without public justification, a move the analyst describes as convenient and dishonest.

Critically, the analyst argues that the sacred cow of public education should not shield the proposal from rigorous scrutiny. Before committing scarce public resources to expanded education funding, policymakers must first answer a fundamental question: what measurable return on public investment do Antiguans and Barbudans expect from expanded education spending? Is the goal to produce more tourism-sector workers, legal professionals, or tech and AI specialists? Without clear outcome metrics, strategic budget allocation is impossible.

Limiting their critique to the funding components of the proposal, the analyst has laid out nine core questions that demand public answers from the government before any vote to extend and expand the tax. These include: what is the annual revenue yield of the current tax, and how is that money currently spent; how much additional revenue does the new education plan require; what happened to revenue from the existing Education Levy; with a total national budget exceeding EC$2 billion, can funds be reallocated from existing priorities instead of raising new taxes; how is the government addressing widespread public sector waste to free up additional revenue for education; how long can the increased tax burden be sustained before it pushes struggling private firms out of business, particularly when they face unfair competition from tax-exempt state-owned enterprises and ongoing global economic shocks; what is the plan to make new education initiatives self-sustaining after the windfall tax is eventually withdrawn; when will state-owned enterprises operating in the taxed sectors start contributing their fair share to the fund, and is it fair to require private firms to compete against state competitors that do not pay the levy; and finally, how will expanded funding guarantee improved education quality, rather than just more spending with no accountability for outcomes.

The analyst rejects Professor Robinson’s framing that policymakers should only focus on what new programs the tax can fund, ignoring the concept of opportunity cost and the growing financial strain already faced by private sector businesses. No discussion has yet addressed how expanding the tax net will push up business costs, which will inevitably be passed on to consumers, already strained by a per-capita annual public spending burden of $20,000. The analyst also questions whether the country can afford to expand public spending programs without risking sovereign fiscal instability.

For the proposal to qualify as a genuine national consideration, the government must first release all relevant data to the public to allow for informed public feedback. Echoing the core principle of democratic governance, the analyst concludes: “No taxation without representation!”