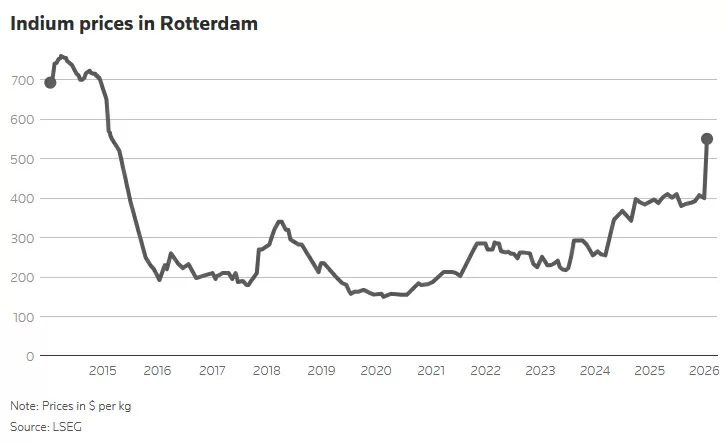

The global market for indium, a critical metal essential for touchscreens, advanced computer chips, and next-generation solar cells, is experiencing unprecedented price surges reaching their highest levels in over a decade. Market data reveals that Rotterdam traders are currently selling indium at $500-600 per kilogram, representing a staggering 55% increase since September of last year.

This remarkable price escalation stems from a convergence of factors: intensified speculative trading on Chinese exchanges, tightening supply from major producers, and growing demand from high-tech and defense sectors. China, which dominated global refined indium production with approximately 70% market share in 2024, has significantly reduced exports. December 2025 figures show China exported merely 22.7 tons of raw indium, marking a 23% monthly decrease.

South Korea, accounting for roughly 17% of worldwide production (180-190 tons out of the global total of 1,080 tons), contributes significantly through major producers like Korea Zinc, which annually sells 90-100 tons. However, production constraints are mounting due to stricter environmental regulations in China, where indium is primarily obtained as a byproduct of zinc ore processing. These environmental policies have curtailed production expansion capabilities, creating structural supply limitations.

The metal’s strategic importance continues to grow across multiple industries. Beyond consumer electronics, indium is crucial for sustainable technologies including high-efficiency solar cells and advanced computing systems. Adding to demand pressures, the U.S. defense sector recently initiated a procurement request for high-quality indium for military applications valued at up to $125 million, signaling recognition of its strategic significance.

Market analysts predict sustained price elevation given the fundamental supply-demand imbalance: constrained production against escalating demand from both commercial and defense sectors. This trend highlights broader vulnerabilities in critical mineral supply chains and the growing geopolitical dimensions of resource security.