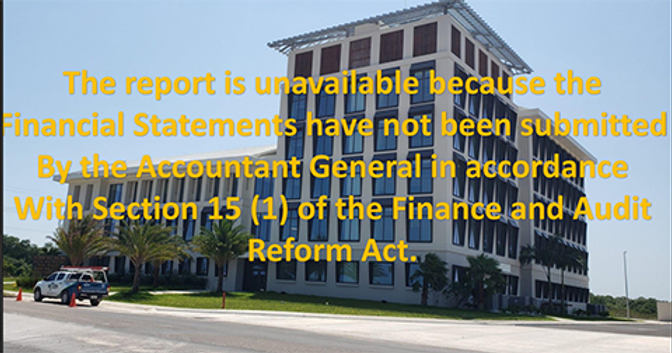

Belize’s accountability framework is facing a severe crisis as the Auditor General’s official website displays only two audit years—2011-2012 and 2015-2016. The absence of annual reports for over a decade has compelled citizens to rely on the Freedom of Information Act (FOIA) to access basic public-finance records. This situation undermines the Westminster-style governance model, where the Auditor General is pivotal in ensuring public accountability by scrutinizing the Government’s financial statements, verifying lawful expenditure of public funds, and reporting irregularities to the National Assembly. These reports, reviewed by the Public Accounts Committee, are essential for maintaining transparency and oversight. However, the constitutional cycle has stalled for more than ten years, with most fiscal years lacking reports due to the Accountant General’s failure to submit required financial statements under Section 15(1) of the Finance and Audit Reform Act. Other years remain unpublished because completed audits were never tabled in the National Assembly, leaving a thirteen-year gap in official reporting. This breakdown has shifted the burden of transparency onto private citizens using FOIA. Public-interest litigant Jeremy Enriquez, for instance, has filed an FOIA request seeking multi-year records on the Constituency Development Fund, including allocations, disbursements, and financial statements for all 31 constituencies. While the Government expressed willingness to disclose the requested material, it requested additional time due to the administrative complexity of compiling records across multiple ministries. Enriquez emphasized that the FOIA mandates an access decision within fourteen days, separate from the time needed to compile documents, and signaled readiness to grant more time once the access request is approved. This situation underscores how the absence of timely Auditor General reports has elevated FOIA from a supplementary tool to the primary means of obtaining financial information.