Jamaica-based property developer First Rock Real Estate Investments has pulled off a notable return to profitability in 2025, driven by skyrocketing rental revenue and upward property value revaluations, but the firm still faces significant headwinds including negative operating cash flow, ongoing debt restructuring and heavy reliance on luxury residential sales to maintain adequate liquidity.

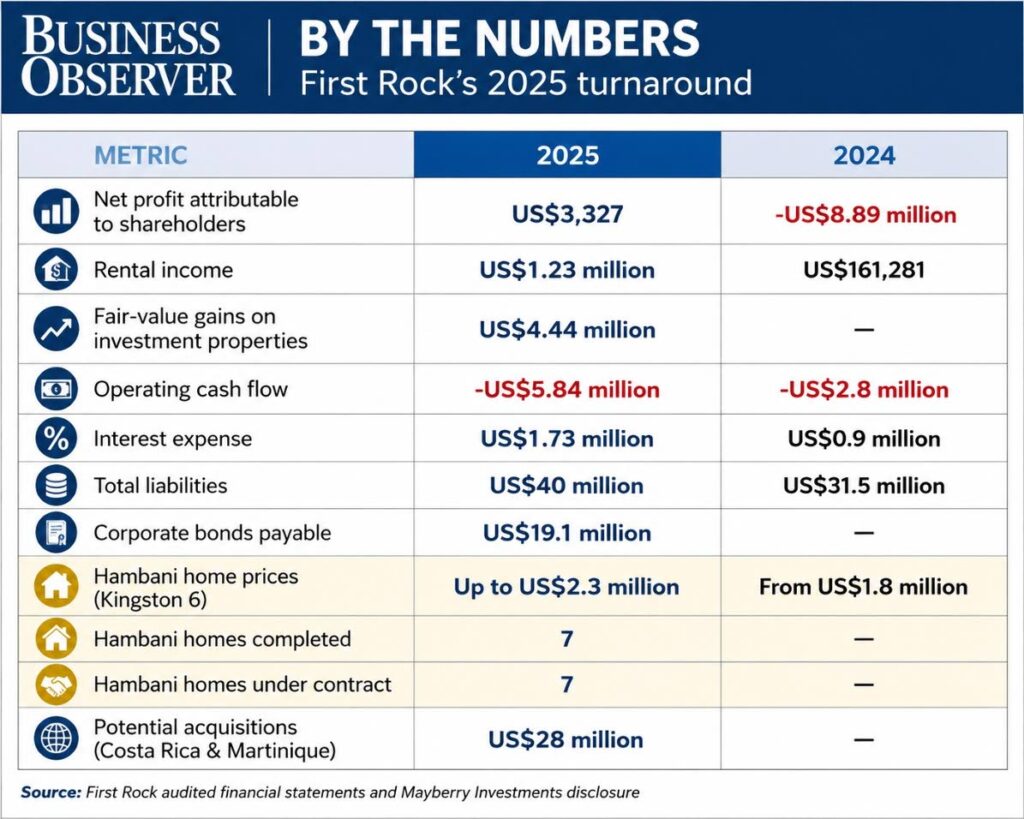

According to newly released financial results, the company logged a net profit of US$3,327 attributable to shareholders for the 2025 calendar year. This result marks a sharp reversal from the US$8.89 million net loss the firm posted in the prior year. The profit turnaround was fueled by two key factors: a 663% year-over-year surge in rental income, which reached US$1.23 million, and a US$4.44 million gain from upward revaluation of the company’s investment property portfolio. Without the non-cash revaluation boost, however, First Rock would still face material earnings pressure, company filings show.

The dramatic jump in recurring rental revenue aligns with First Rock’s publicly stated strategic pivot toward stabilizing commercial and income-producing real estate assets, a move designed to cut the firm’s historical reliance on one-off development project sales. Even with this top-line improvement, audited financial statements reveal ongoing strain on the company’s cash position. Operating cash flow registered a negative US$5.84 million for the year, while annual interest expenses nearly doubled to hit US$1.73 million amid a broader high interest rate environment that has pushed up financing costs across the global and local real estate sectors. First Rock remains in active negotiations with creditors to refinance maturing short-term debt and secure additional working capital to fund its ongoing operations.

At the center of the firm’s near-term cash generation strategy is the near-completed Hambani luxury residential development located in Kingston 6. In a disclosure dated April 30, transaction advisor Mayberry Investments confirmed that seven luxury villas at the development have received practical completion certificates, and all seven are already under contract to buyers. Completed units are priced between US$1.8 million and US$2.3 million, and Mayberry noted that proceeds from sales to date are enough to cover all remaining development costs and leave a surplus of cash to support other corporate obligations.

First Rock Chief Executive Officer Ryan Reid explained that the company’s current capital structure was intentionally structured to tie debt repayment timelines to development completion and unit sales. “Unit sales are indeed a key part of our repayment strategy, and that’s really by design, which reflects the direct alignment between our development pipeline and our capital structure,” Reid told the Jamaica Observer in written comments.

A review of the company’s balance sheet shows 15% year-over-year expansion in total assets, which grew to US$65.8 million at the end of 2025. Total liabilities also climbed, rising from US$31.5 million in the prior year to US$40 million in 2025. Outstanding corporate bonds jumped sharply to US$19.1 million, while combined current and non-current long-term loans remained elevated at roughly US$16 million. Audit notes reveal that some of First Rock’s newest financing arrangements carry interest rates as high as 18%, underscoring the steep cost of capital facing heavily leveraged property developers operating in Jamaica’s current high interest rate landscape.

Reid emphasized that growing recurring rental revenue will be the core driver of improved operating cash flow going forward. “The revaluation gains reflect genuine value creation in our portfolio, but we absolutely understand that cash generation is important, hence the massive movement in our rental income year on year,” Reid told Business Observer. “We expect operating cash flow to further improve meaningfully.”

Even as the company works through ongoing debt refinancing discussions, First Rock is advancing plans for two regional acquisitions in Costa Rica and Martinique, with a combined transaction value of US$28 million. Reid stressed that the planned purchases are not aggressive expansion into speculative development, but rather a targeted move to accelerate growth in recurring cash flow. “The acquisitions we’re pursuing are not about expansion for its own sake, they are highly selective opportunities that we believe will generate returns faster than greenfield developments would. These are fully tenanted rental income opportunities,” Reid said. “In each case, the entry price, existing entitlements, and near-term development potential mean these assets contribute to cash generation rather than stretching it further.”

Auditors from Ernst & Young, the firm that signed off on First Rock’s 2025 financial statements, identified investment property valuation as a key audit matter. They noted that investment properties and properties held for sale collectively account for roughly 50% of the company’s total assets as of year end. After years of debt-fueled expansion, First Rock now faces growing pressure to prove that its evolving rental-focused business model can generate sustained, stable cash flow, reducing the firm’s current heavy reliance on non-cash property revaluations and irregular development sales to deliver positive bottom-line results.